Mark Leonard, the founder and visionary behind Constellation Software, has been serving as CEO since the company’s inception in 1995, quietly shaping a unique success story. Despite his status as one of the lowest-profile billionaires in the business world, Leonard’s impact and capital allocation skills cannot be emphasized enough. His journey began with a decade-long stint in venture capital, during which he recognized the untapped potential of small VMS firms. This realization laid the foundation for his distinctive approach of building a growth engine around these underappreciated companies.

Constellation operates across a diverse spectrum of over a hundred distinct verticals, encompassing a portfolio that spans several hundred companies. Owing to this diversified corporate framework, no individual business unit or segment holds material significance for the organization.

Maintenance and other recurring revenue (71% of fiscal 2022 sales) primarily consist of fees from customer support on software products post-delivery and include recurring fees earned through Software-as-a-Service products. Professional service revenue (21%) comes from fees charged for implementation services, custom programming, product training, and consulting.

We believe the secret sauce in Constellation’s competitive edge lies in the culture that characterizes its acquisition approach. It aims to be a perpetual owner of the acquired companies, thereby distinguishing the business from conventional private equity firms whose primary focus is the subsequent resale of their acquired assets at a premium in the future.

Notably, the firm acquires over 100 companies each year (averaging one every other business day). This pace is only possible in a decentralized decision-making framework, which also includes the critical function of capital allocation. Constellation’s corporate headquarters grants significant autonomy to subsidiary management levels, empowering them with the authority to evaluate potential acquisition targets and make informed decisions based on their assessments.

We believe another pillar of Constellation’s moat lies in the characteristics of its portfolio members. Essentially, it’s a conglomerate composed of an army of small but moaty businesses, each characterized by high switching costs. In essence, VMS companies provide highly customized solutions to meet the needs of a specific segment.

Although we do not favor serial acquirers in general (as this feature seldom aligns with consistent shareholder value creation), we hold the conviction that Constellation’s attributes justify the designation of a wide-moat enterprise.

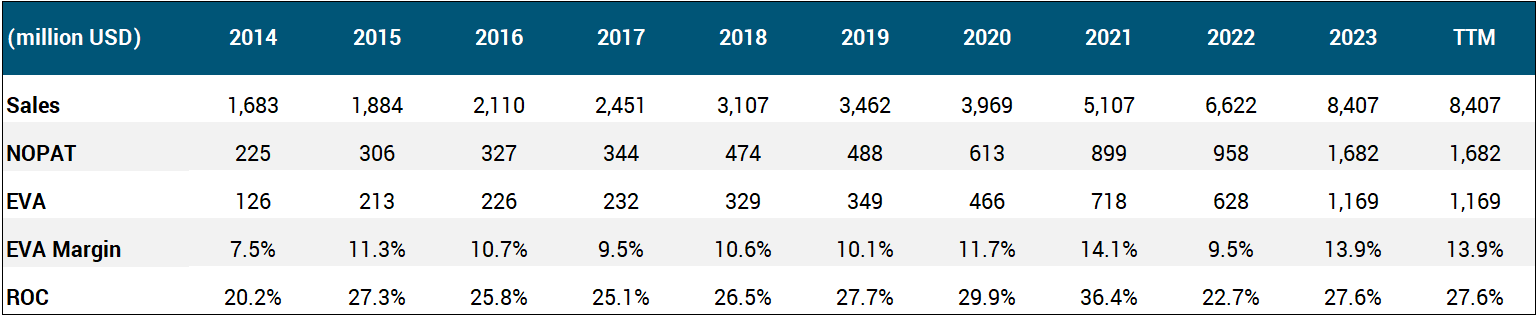

As for the future, it is worth noting that the collective organic growth rates exhibited within Constellation’s portfolio of companies have been rather modest, yielding a low-to-mid-single-digit annualized CAGR over recent years. Consequently, Constellation’s growth engine can be best understood by the principle that a firm’s long-term annualized earnings growth rate converges to its reinvestment rate times the return on its incremental invested capital. Assuming that Constellation can continue allocating 80% of its internally generated cash (NOPAT) each year at 20%+ ROC levels, we arrive at a strong double-digit inorganic revenue and earnings growth potential.

At its core, this firm can be characterized as a capital-light compounder because the VMS businesses under its umbrella require very little reinvestment. Then, recurring cash flows generated by the VMS firms are harnessed to fuel a relentless acquisition engine, resulting in consistently stellar ROC levels in the 25-30% range.

Turning to shareholder distributions, Constellation pays a tiny, negligible regular dividend. In 2019, shareholders received a sizable, ~$18 per share special dividend due to the lack of attractive redeployment opportunities. Constellation has garnered a unique shareholder base that would prefer Leonard to reinvest this money instead of distributing it. Therefore, we find it unlikely that another special payout will take place in the foreseeable future, and even the ordinary dividend could be sacrificed if a better use of cash presents itself.

Looking at the stock’s valuation, Constellation’s shares have always appeared pricey on the surface. Regardless, its EVA growth over the past 5-10 years has managed to surpass even the market’s rosy expectations. Please see below the valuation metrics of the EVA framework that remedy accounting distortions to give us a clearer picture on where the stock stands in a historical context.

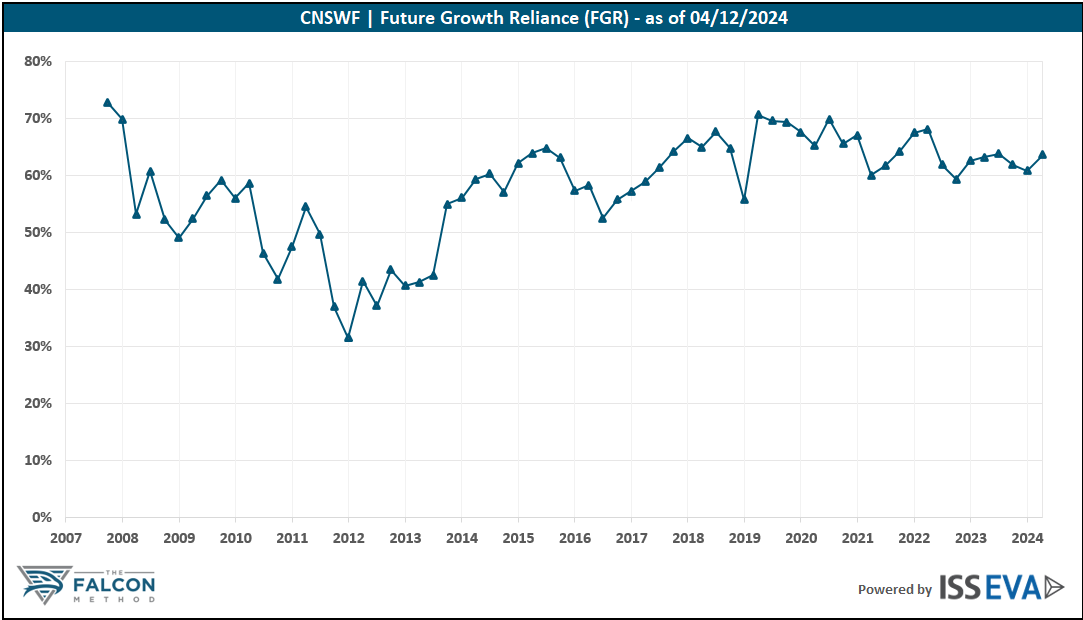

The “fair” valuation range in the future hinges on the firm’s reinvestment efficiency, and as we see potential downside risks on the growth front, we have employed more conservative assumptions in our model. Nevertheless, the market-relative valuation seems unattractive at the moment with a NOPAT yield of 2.8%. Waiting for the valuation component to become at least neutral to the total return formula seems a reasonable approach at this point.

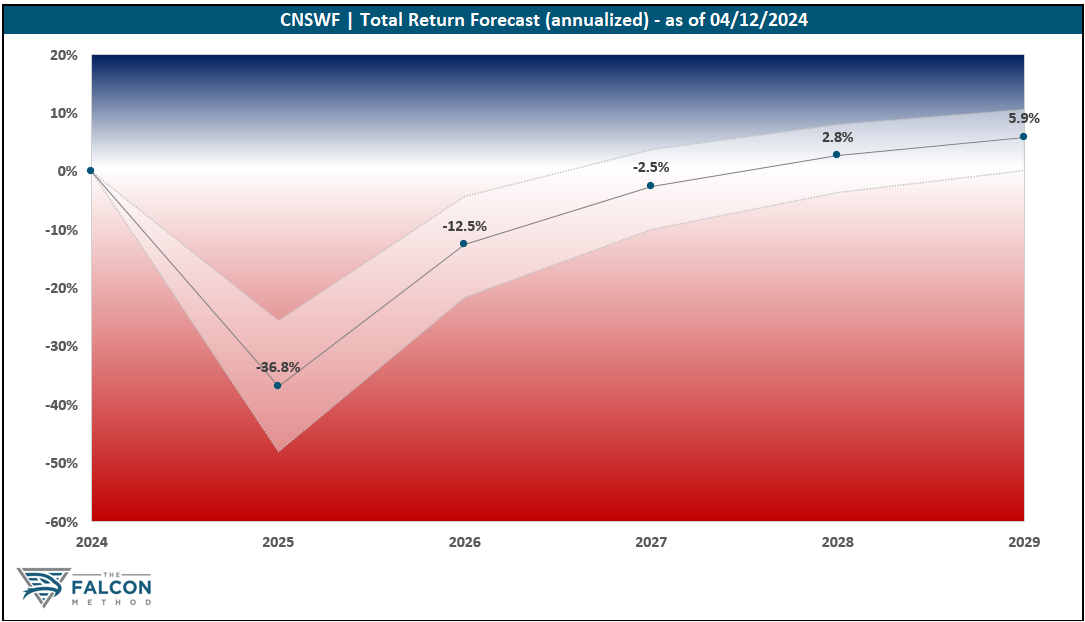

Overall, the time to get excited is not now. The “Key Data” table and the 5-year total return potential chart speak for themselves.

The FALCON Method can identify much better opportunities in the current market, so we are passing up on Constellation for now.