I’m a practical guy, so let’s start with two case studies:

These will make it easier to understand the logic behind the two different kinds of stocks: Fallen Angels and EVA Monsters.

(If you haven’t already, please read my articles about commonly used multiples and EVA, the most demanding profit score.)

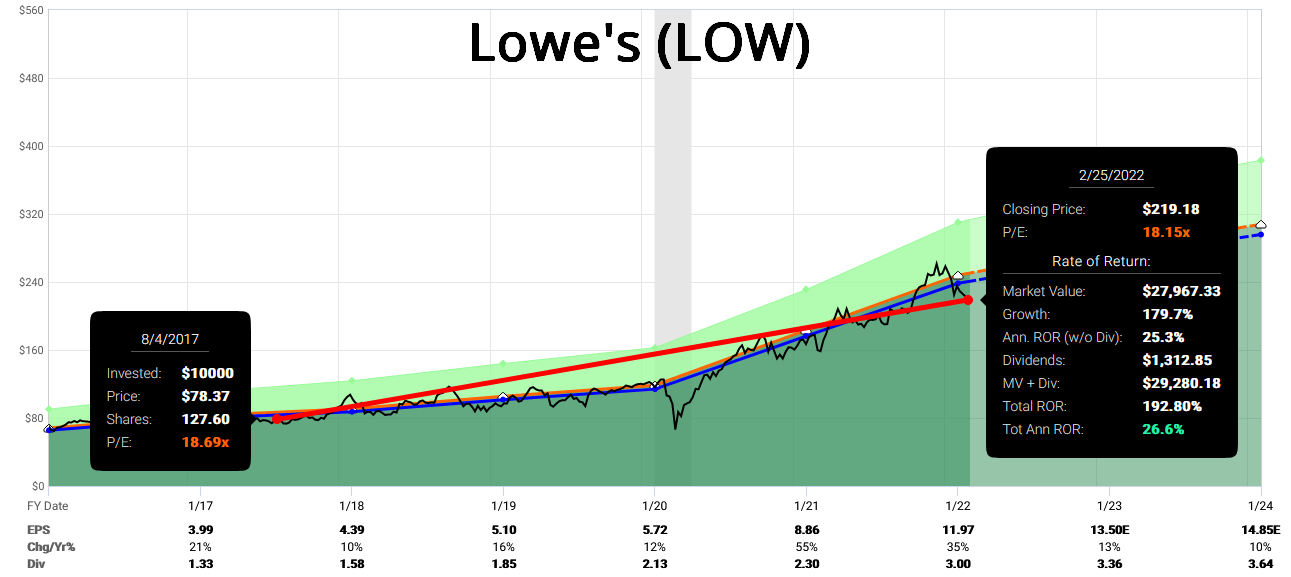

I bought Lowe’s (LOW) stock on August 4, 2017, at $78.37. As things stand, this investment has produced a ~27% annualized return in 4.5 years, and I’m still holding the shares.

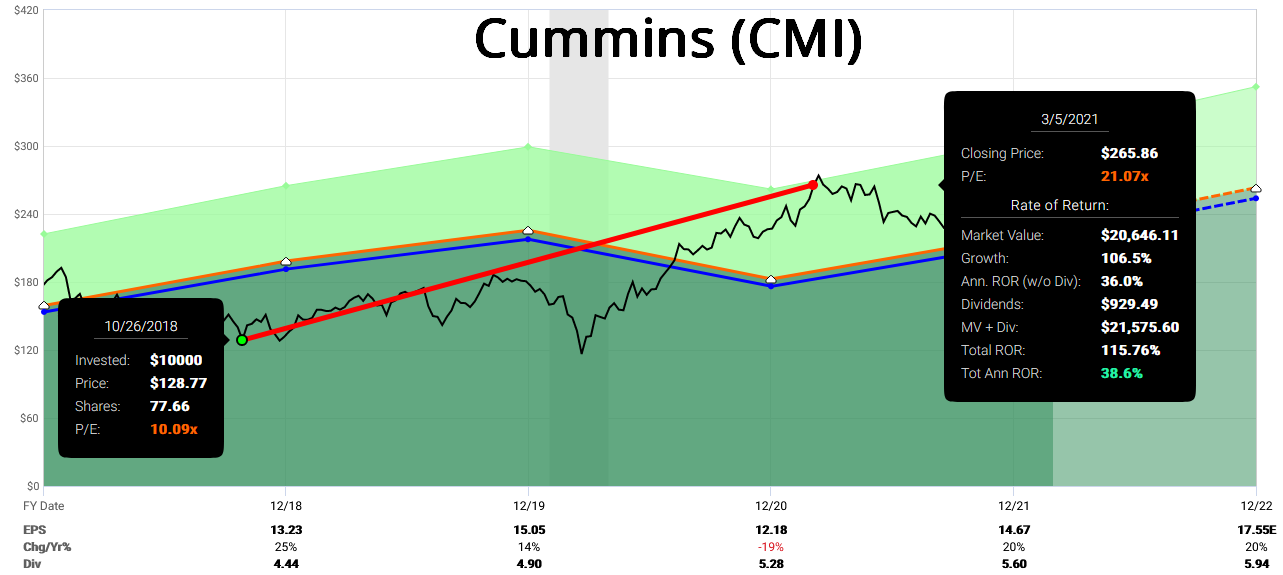

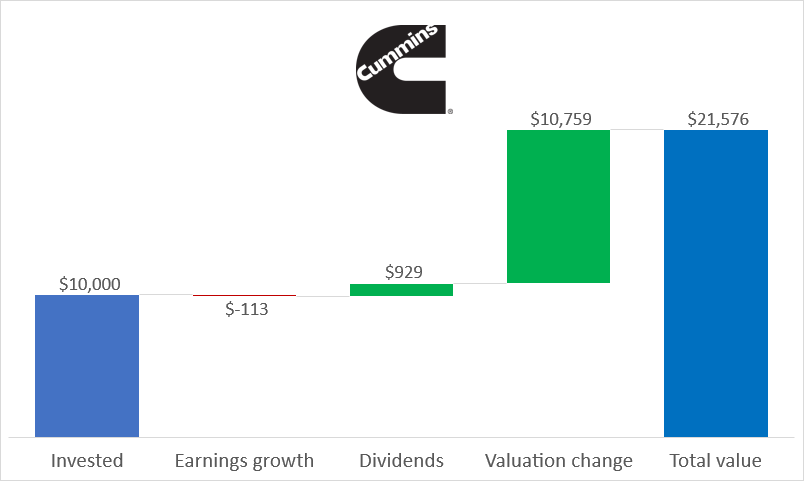

The second example is Cummins (CMI), which I bought on October 26, 2018, at $128.77 and sold at $265 on March 5, 2021, pocketing an annualized return of ~39%.

Source: FAST Graphs

There was a reason for selling the latter stock while holding on to my Lowe’s position. You’ll get it very soon.

Although the returns look great in both cases, Lowe’s and Cummins are two very different types of investment, and this is exactly what I’d like you to understand.

Why were these returns so high?

When you hold a stock, you can make money from two sources: the price can go up, and you can collect dividends. There is no other way!

To take it a step further, we can break up the stock appreciation part into two components: earnings growth and price-to-earnings (valuation) expansion/contraction.

So the comprehensive total-return formula looks like this:

Total return = Earnings growth + price to earnings expansion + dividends

Now back to the question: what drove those eye-catching returns in the two examples?

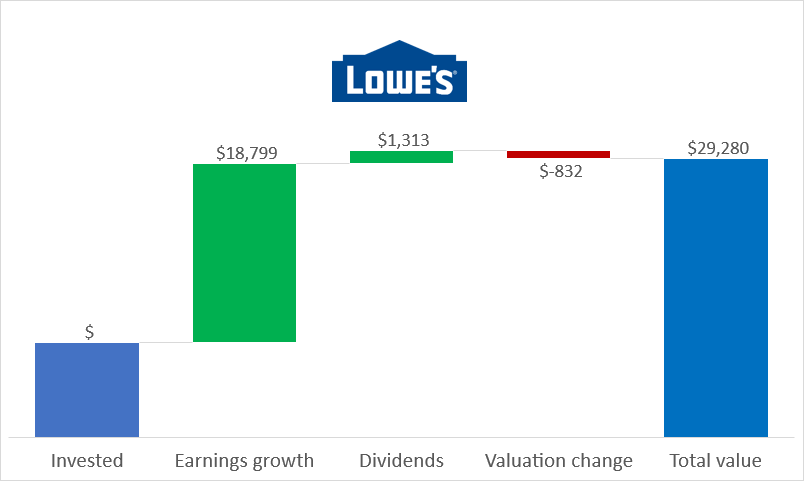

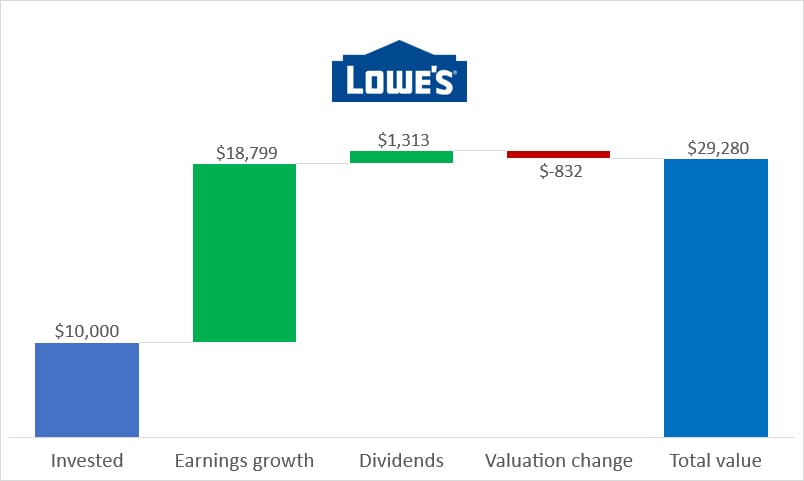

In Lowe’s case (the stock I held onto), the earnings per share almost tripled, while the PE multiple actually contracted somewhat (acting as a headwind), and we harvested growing dividends along the way.

Here is how the combination of these factors worked: (Adding up the first 4 columns equals the total value)

It is obvious that the company’s earnings growth drove my investment return with Lowe’s. Now let’s see how the Cummins position worked. (The stock I sold.)

While Cummins’s earnings grew nothing during my holding period, I received ~9% of my invested capital in the form of dividends in those ~2.5 years, and the expansion of the valuation multiple did the heavy lifting to contribute the lion’s share of my returns.

Jumping ahead…

What on earth could have made me hold on to my Cummins stock after the valuation corrected upwards while the company didn’t show any sign of growth?

The best part has already happened!

The valuation became high, and without the business growing, I could not expect exceptional returns in the future.

On the other hand, selling Lowe’s would be a costly mistake even at a seemingly stretched valuation (high PE). And this gets us to the point that not all stocks are equal, and different types may need different treatment when it comes to analysis and decision-making.

Read on, and get the insight that took me 10+ years to grasp…

EVA Monsters and Fallen Angels

In pursuit of maximizing total returns, two segments of the stock universe are of exceptional importance, which we simply refer to as “EVA Monsters” and “Fallen Angels.”

The fundamental return of every stock (excluding the effect of valuation) is composed of:

Fundamental Return = Profit (EVA) CAGR + dividend yield + share count reduction

In the case of the aforementioned two categories, the composition of fundamental return is very different:

1. EVA Monsters:

These are high EVA-growth companies, where the majority of our fundamental return stems from future growth in EVA. Some of these companies are major repurchasers of their shares, and most pay no dividends since they have wonderful reinvestment opportunities.

2. Fallen Angels:

These are mature businesses that have stable EVA generation capability but lackluster growth. Most have a sizable dividend payout, potentially enhanced by share repurchases.

While both types of investments can yield handsome results, it is readily apparent that “EVA Monsters” have a higher fundamental return than “Fallen Angels” because they possess much better growth characteristics.

Why is fundamental return important? Because the longer you hold a stock, the closer your return will get to this fundamental return.

As Charlie Munger put it:

“Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns.“

In short: when our aim is to hold a stock for decades, we want “EVA Monsters” in our portfolio.

Once we have laid this foundation, we can introduce valuation as the last missing piece of the equation. Let’s see the full investment thesis behind both groups:

Total Return = Fundamental Return + Change in Valuation

In the case of “Fallen Angels,” sentiment change is the primary source of total return. Since reversion to the mean is a one-trick pony, the sooner it happens, the higher our annualized return.

The most dangerous pitfall is that this reversion takes too long to happen (if at all), dampening our total return since there is no growth to compensate for the time elapsed.

A company can offset some of the “waiting time” with a handsome dividend payout, assuming the dividend is sustainable and that the EVA generation is stable.

Simply put: when we buy “Fallen Angels,” we want a huge discount to fair value coupled with a short holding period, hoping for a quick rebound in valuation.

Until then, we collect the dividends, and when the reversion takes place, we sell at fair value (the sooner, the better).

In a nutshell, we don’t want to be stuck holding a “Fallen Angel” for too long unless it turns into an EVA Monster along the way (which is rather unlikely but cannot be ruled out).

Monitoring these positions closely is absolutely essential since some of them may turn out to be value traps while others may transform into EVA Monsters.

When it comes to “EVA Monsters,” we want to buy companies with lots of EVA growth left in the tank, at a reasonable entry price and hold them for the long run.

The primary pitfalls are that we either overpay for growth or the forecasted growth does not materialize to the extent we expected. Both scenarios would sink our total return potential.

Thus, we have to leave a buffer in our purchase price in case some of the EVA growth we had anticipated does not materialize, which is painful in not one but two ways:

- the significantly dampened fundamental return

- and the corresponding change in market sentiment (that affects the valuation component of the equation), to adjust for lower future growth.

Back to the case studies

While the quality and growth factors played the most important part with EVA Monsters, it is the valuation that drives returns with these once-beloved dividend darlings that landed in the bargain bin. This describes perfectly why we call this category Fallen Angels.

As a reminder of our case study, you can see how different components of the total return formula played the key role in Lowe’s and Cummins’ case, where the former classifies as an EVA Monster while the latter was a Fallen Angel investment.