In 2007, Peter Gassner founded Veeva as a verticalized Customer Relationship Management business built on top of Salesforce and custom-made for the life sciences industry. Gassner had the original insight while working at Salesforce as VP of Technology and saw their limitations as a horizontal platform. He profoundly impacted the pharma industry by introducing a brand-new SaaS solution to the market, and he has been serving as CEO ever since Veeva’s founding.

Subscription fees are Veeva’s primary revenue source, contributing 80% to the top line as of fiscal 2023. These fees encompass Software as a Service (SaaS) revenues, roughly evenly distributed between commercial and R&D offerings.

Veeva Commercial Cloud represents a product family comprising software and data services tailored specifically for life sciences companies aiming to enhance the efficiency and effectiveness of their product commercialization processes by offering solutions for sales, medical affairs, and marketing functions. Conversely, the firm’s R&D solutions target the clinical, regulatory, quality, and safety functions, assisting life sciences companies in streamlining their end-to-end product development processes. This, in turn, promotes increased operational efficiency and ensures regulatory compliance throughout the product life cycle.

While its customer base is concentrated in the biopharma industry, Veeva serves a diverse array of over 1,000 enterprise clients. These range from the largest global pharmaceutical and biotechnology firms, such as Eli Lilly, Gilead Sciences, and Merck, to emerging startups in the field.

Veeva has established a moat around its business by differentiating itself from generic Customer Relationship Management (CRM) providers. Specializing in the life sciences industry, the firm embodies all the characteristics of a typical Vertical Market Software (VMS) provider. Generally, such solutions handle mission-critical applications in their clients’ businesses, thereby incurring substantial switching costs.

What distinguishes Veeva is its highly cohesive product ecosystem, spanning from commercial (cloud, data, analytics) to R&D solutions (clinical, quality, regulatory, safety). In essence, Veeva’s platform consolidates traditionally siloed and disconnected workflows, enabling its customers to manage the entire lifecycle of a clinical trial, from molecule discovery to commercialization. While competitors do offer some similar solutions, no product on the market can match the firm’s comprehensive platform, which is its primary advantage.

Because the total cost of Veeva’s software suite amounts to approximately 1% of its customers’ annual revenue, there is little incentive to switch to a competing solution and potentially risk business disruption. The company’s retention rate has exceeded 100% over the past few years, indicating that its customers not only renew but also increase their purchases each year, with few subscription cancellations.

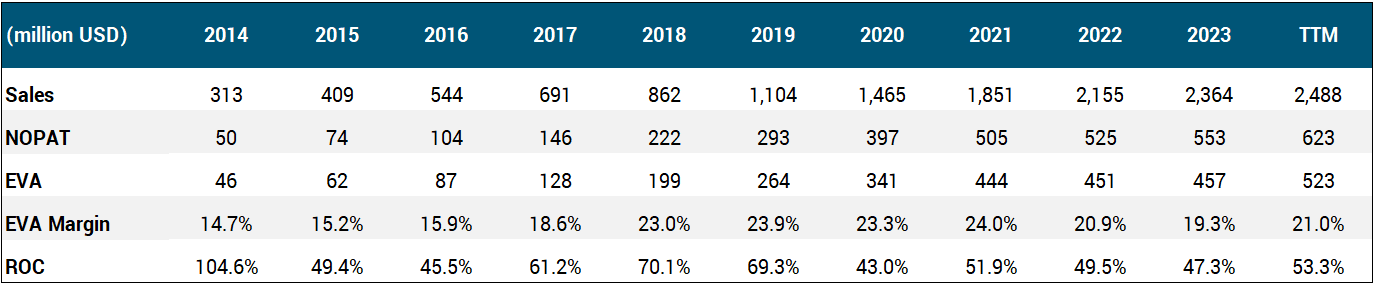

Overall, the company undeniably deserves a wide-moat classification from a qualitative standpoint. It also excels in meeting our quantitative criteria, displaying robust double-digit ROC and EVA Margin figures. Alongside evident pricing power and a lucrative clientele, the underlying dynamics in life sciences contribute to these outstanding profitability metrics.

As for the future, Veeva’s life sciences end markets represent a large and growing pie, with the biopharma and medical technology sectors estimated to expand at a mid-single-digit annualized rate over the long run. Industry-specific software and data solutions will likely exhibit higher growth rates as the segment becomes more technologically enabled. The firm’s prospective customers are eager to replace their in-house legacy software or general-purpose CRM tools with Veeva’s cloud-based solutions focused on life sciences. According to management, the firm has penetrated just over 10% of its addressable market, leaving ample room for future share gains.

Turning to capital allocation, Veeva typically reinvests about 40% of its internally generated cash and achieves magnificent ROC figures north of 50%. R&D is generally the most significant use of capital as the company continues to release new product categories (like Vault and QualityOne) and add-on modules, paired with smaller, tuck-in acquisitions that management considers complementary to the product portfolio.

The picture is pretty bleak on the shareholder distribution front. Veeva has never paid a dividend (which is unlikely to change anytime soon), and it has spent only a negligible amount on share buybacks since its IPO. This has two consequences. (1) As the reinvestment rate is below 100%, and virtually no money is returned to shareholders, the firm’s cash balance has grown from $300 million in 2014 to over $4 billion as of today. (2) The share count keeps rising due to the dilutive effect of employee equity grants, increasing by ~13% in aggregate since the IPO. Despite management’s indisputable “efficiency focus,” Veeva is granting enormous stock-based compensation packages, resulting in an average annual dilution of over 2% per annum (way above our not-so-strict threshold of 1%).

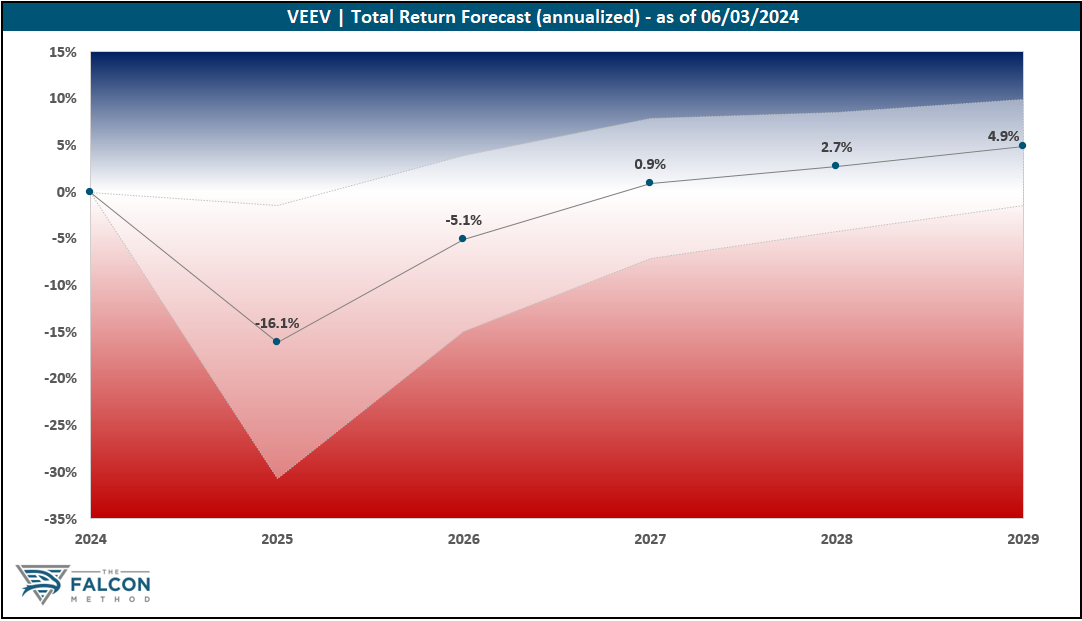

Looking at the stock’s valuation, in Veeva’s case, we don’t consider historical multiples to be a good forward-looking proxy, given the company’s material increase in size over the past 5-10 years, while its growth rate has (naturally) come down. Please see below the valuation metrics of the EVA framework that remedy accounting distortions to give us a clearer picture on where the stock stands in a historical context.

Regardless of how we look at it, the stock appears very expensive on a market-relative basis with its 2.6% NOPAT Yield. The 10-year baked-in EVA growth is also near 20% at the current price, which we deem extreme.

Overall, the time to get excited is not now. The “Key Data” table and the 5-year total return potential chart speak for themselves.

The FALCON Method can identify much better opportunities in the current market, so we are passing up on Veeva for now.