Siegfried Meister founded what is now Rational AG in 1973. For 44 years, he led his life’s work to success and remained true to his motto of focusing on customer benefit. Although he passed away in 2017, his values are still firmly embedded in the corporate culture today. His dear friend, Walter Kurtz, also played a crucial role in turning Rational into a success story, and he still holds a significant ownership stake in the business.

The majority of Rational’s top line (70% as of fiscal 2023) comes from the sales of its multifunctional cooking systems. The flagship product is called iCombi Pro, a combi-steamer with intelligent, software-controlled cooking paths, where heat is transferred by steam and hot air to achieve the desired result. The remaining portion of the company’s top line (30%) stems from aftermarket sales, including accessories, spare parts, and maintenance services for its cooking appliances.

Rational has long been a pioneer in its field, establishing the combi-steamer category almost 50 years ago. Ever since, the firm has remained the global market and technology leader in innovative solutions for thermal food preparation in the world’s professional kitchens, boasting a market share of around 50%, roughly five times greater than its closest competitor.

Even though the purchase of a combi-steamer represents a significant capital outlay for its clients, it is widely regarded as an investment with exceptional returns, resulting in payback periods of just a few months and ROI figures well over 100%, which explains the relentless demand for Rational’s appliances.

Additionally, Rational’s appliances have a reputation for reliability and German quality, coupled with a market-leading warranty program. The firm also offers a global service network with 24/7 availability, enabling it to minimize expensive downtime for its clients. Rational has stayed at the forefront of innovation for decades, allocating 5% of its sales on average toward R&D.

Overall, despite being a significant investment from its customers’ side, Rational’s ecosystem and its array of value-added offerings represent a lower total cost of ownership compared to traditional appliances and competitors. compared to traditional appliances and competitors.

As for the future, as prosperity increases worldwide, the restaurant and catering sector gains more importance because it materially contributes to the standard of living for the expanding global middle class. Consequently, the number of quality meals that need to be prepared every day around the world continues to grow. All of this results in the restaurant sector growing at a GDP-beating pace for years to come, serving as a baseline growth rate for appliance suppliers as well.

We argue that Rational will likely continue to outgrow the broader market, propelled by the powerful tailwind of combi-cookers replacing traditional technology in professional kitchens. Based on management’s estimates, there is ample untapped market potential for both of its product groups, with iCombi and iVario serving roughly 12% and 2% of their addressable markets, respectively.

As for capital allocation, Rational typically operates with a very low reinvestment rate of 10-15%, while ROC figures have averaged a staggering 45%. The company also maintains a very solid balance sheet with more than sufficient liquidity and zero debt.

As for shareholder distributions, since the business requires minimal incremental capital to operate and grow, most of the surplus cash can be paid out as dividends. Although the firm has declared a payout every year since its IPO, the amount has been quite irregular because management adheres to a 70% payout ratio, regardless of the yearly profit. Special dividends have also been occasionally announced when there was no better use of cash.

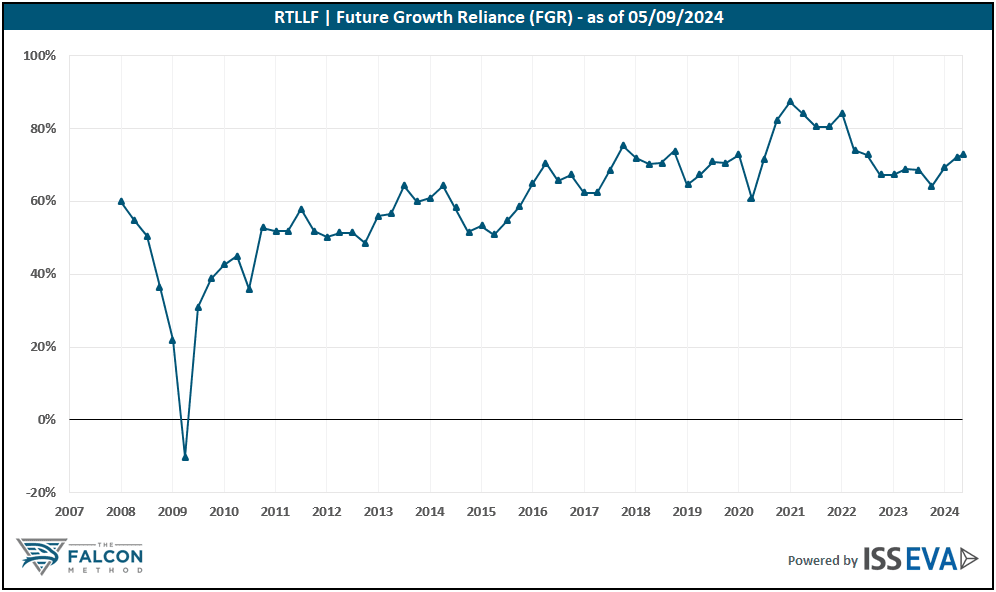

Looking at the stock’s valuation, Rational’s stock has always been extremely highly rated, except during market downturns like the 2008-09 recession or the COVID crisis in 2020. In other words, if you look solely at the growth characteristics of the business, you could have seldom bought this stock at a seemingly sensible valuation. Please see below the valuation metrics of the EVA framework that remedy accounting distortions to give us a clearer picture on where the stock stands in a historical context.

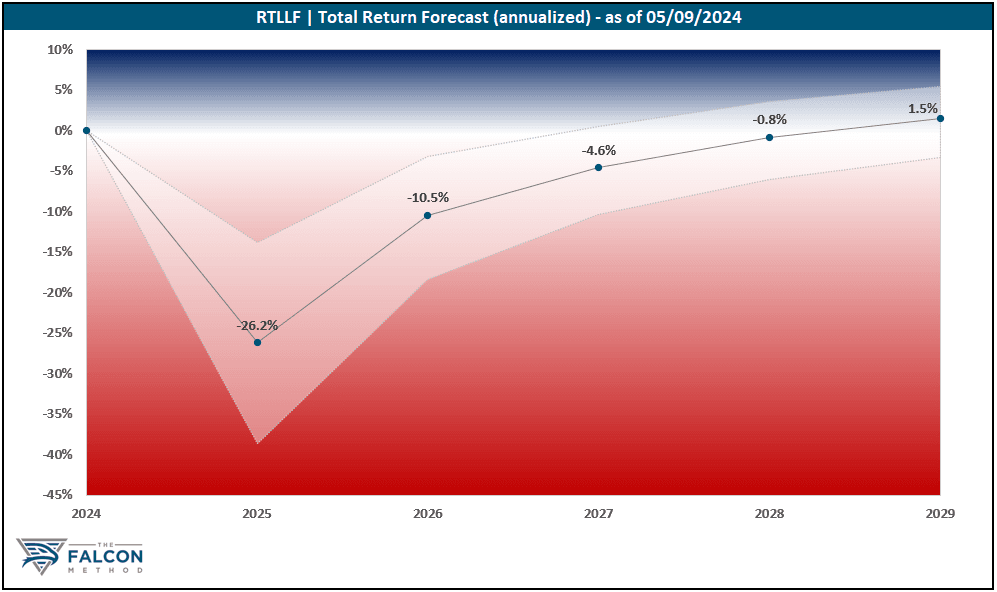

At this price, the market anticipates a 20% EVA growth annually over the next 10 years, which is nearly impossible to justify. The 2.4% NOPAT Yield is also starkly below the market average of 4.0%.

Overall, the time to get excited is not now. The “Key Data” table and the 5-year total return potential chart speak for themselves.

The FALCON Method can identify much better opportunities in the current market, so we are passing up on Rational for now.