From the Closing Thoughts of the January 2023 FALCON Method Newsletter (published on 08/01/2023)

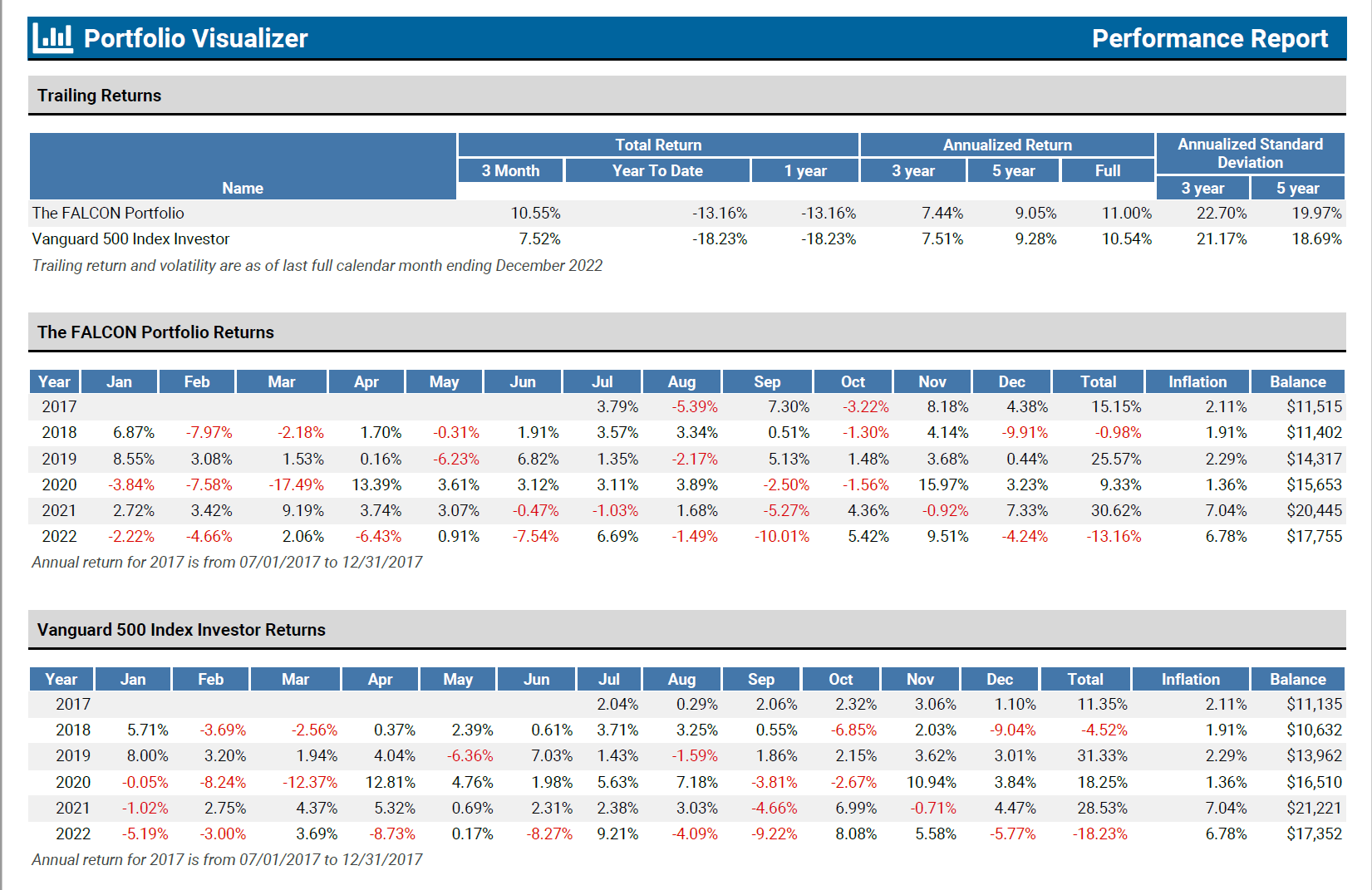

The numbers are in. As usual, in the January issue, we take a look at how our FALCON Portfolio has performed relative to some benchmarks. To make this comparison fair, we had to ditch Old School Value’s (OSV) calculator and switch to Portfolio Visualizer Pro. While I now consider this latter tool the golden standard of performance evaluation (mainly because of its transparency), OSV’s solution served us well through the years.

The reasons for switching were plenty: (1) Eaton Vance got acquired, and its ticker symbol ceased to exist, which OSV couldn’t properly handle. (2) OTC stocks are not supported by OSV, so we had to find a workaround for including Tencent in our modeled portfolio, just like we had to come up with a creative solution to address the Eaton Vance issue. The more tinkering it required, the less reliable the results became. (3) OSV seems to be applying daily rebalancing when modeling an equal-weighted portfolio, and that frequency is simply unrealistic. (4) Last but not least, dividends are added to portfolio returns in OSV, but it cannot handle dividend reinvestments, which significantly distorts long-term results when compared to total return indexes (that benefit from the impact of continuously reinvested dividends). All in all, Portfolio Visualizer Pro transparently shows that the newsletter’s performance may have been underreported until now, mainly due to reason #4.

Without further ado, our FALCON Portfolio’s value decreased by 13.2% in 2022, outperforming both the S&P 500 (-18.1%) and the MSCI World (-17.7%). This is no surprise since our defensive strategy tends to lose less when the market falls, thus preserving a higher base to build on once the tide turns. Of course, defensiveness also means we are not capturing 100% of the upside amid euphoria, but the numbers do work out over cycles. (More specifically, we have a downside capture ratio of 96.4% and an upside capture ratio of 98.5%.) Since inception, our newsletter’s equal-weighted portfolio has produced an annual return of 11.0%, compared to the S&P 500’s 10.7% and the MSCI World’s 8.1%. All figures include reinvested dividends. You can see our report card below, showing all our monthly, annual, and cumulative returns. (The numbers speak for themselves; not that I was too interested in the monthly breakdown.)

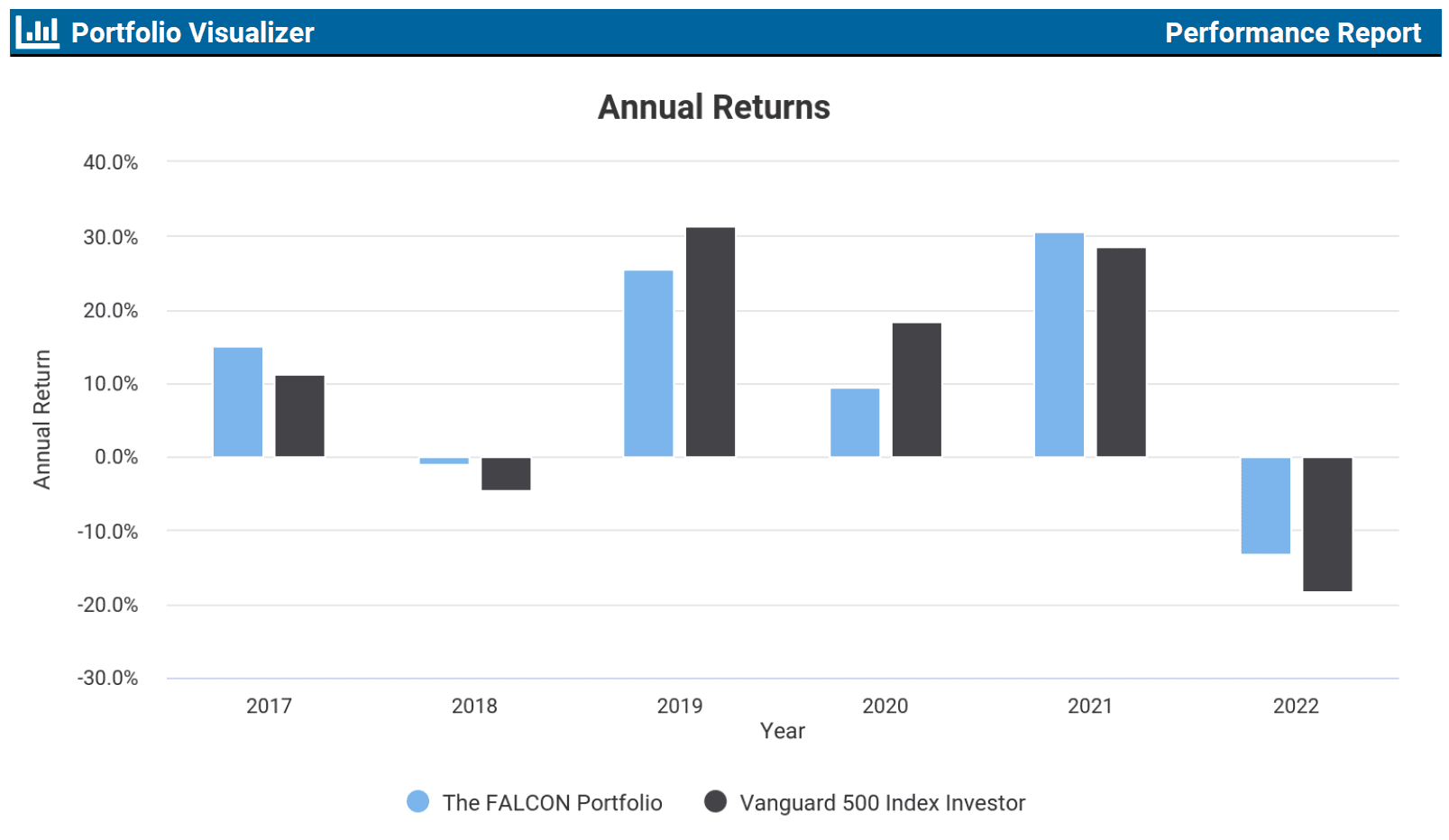

I consider the interpretation much more important than the outcome, so allow me to spill some virtual ink on this topic. I have long said, and results do prove that our investment strategy is defensive in nature, so we expect to generate most of our alpha during down markets. (Those down markets that have failed to materialize for a while.) Check this chart of annual returns to see what I mean.

Some may argue that our EVA Monster focus tilts us toward a more aggressive approach, and it has most certainly increased our downside capture ratio. Yet I want you to understand that our quality-growth picks are highly profitable companies with enviable market positions. Consequently, we are not investing in your typical speculative growth stock that not only got slaughtered as yields rose but may have trouble regaining footing until turning profitable and cash flow positive. All in all, I’m happy with the blend of two stock types in our portfolio: dividend-paying Fallen Angels and quality-growth beasts that go by the EVA Monster name.

When it comes to performance evaluation, a not-too-often quoted piece by Bill Miller may be thought-provoking. In his 2005 letter, Miller writes: “You are probably aware that the Legg Mason Value Trust has outperformed the S&P 500 index for the past 15 calendar years. That may be the reason you decided to purchase the fund. If so, we are flattered, but believe you are setting yourself up for disappointment. While we are pleased to have performed as we have, our so-called ‘streak’ is a fortunate accident of the calendar. Over the past 15 years, the December-to-December time frame is the only one of the twelve-month periods where our results have always outpaced those of the index. […] We would love nothing better than to beat the market every day, every month, every quarter, and every year. Unfortunately, when we purchase companies we believe are mispriced, it is often difficult to determine when the market will agree with us and close the discount to intrinsic value.” The only reasonable goal can be to construct an investment portfolio that has the potential to outperform the market over entire business cycles.

And were I not a newsletter provider, I wouldn’t even bother about outperforming any benchmark. By all means, please read Morgan Housel’s “Internal vs. External Benchmarks” post to get the message. Just a short quote, as I guess that 99% are not clicking on any links: “The only way to consistently do what you want, when you want, with whom you want, for as long as you want, is to detach from other people’s benchmarks and judge everything simply by whether you’re happy and fulfilled, which varies person to person. I recently had dinner with a financial advisor who has a client that gets angry when hearing about portfolio returns or benchmarks. None of that matters to the client; all he cares about is whether he has enough money to keep traveling with his wife. That’s his sole benchmark. ‘Everyone else can stress out about outperforming each other,’ he says. ‘I just like Europe.’ Maybe he’s got it all figured out.”

Turning to the macro picture, 2022 was undeniably dominated by the Federal Reserve’s actions to fight inflation. The latest 0.5% increase was anticipated, but the expected terminal rate of 5.1% (equivalent to a target range of 5%-5.25%) by the end of 2023 moved up from the 4.6% projected by the Fed back in September. As things stand, seven central bank officials expect rates to go even higher, with two seeing rates topping out at 5.75%. One hawkish official expects rates to remain at that level through 2025. Chairman Jay Powell said it was impossible to know if a recession would occur, and if one does, how long it would last or how deep it would be.

I believe the stock market has been focusing on an optimistic inflation scenario throughout 2022, yet defensive sectors have performed well. This may change quickly if the outlook begins to improve. I read that in the latest Barron’s poll of Wall Street strategists, not one 2023 target suggests a loss in the S&P 500 over the coming year. The average year-end target for 2023 is above 4,200, with both the median and average target implying a 2023 total return of over 10% for the index. I’d be itching to hear the expert explanations, given that valuations at the top in early 2022 were higher than those of 1929 and 2000, interest rates are significantly higher than any period from 2009 to 2022, and inflation is higher than any point in the last 50 years. With that being said, our FALCON Portfolio is an all-terrain vehicle that will serve us well whatever comes in 2023 and beyond. Be patient, stick to the plan, and enjoy every minute of the journey!

New to the FALCON Method? Check out how our investment process works: How to Build an Evidence-based Stock Selection Process in 7+1 Steps