Summary

- Investing the Warren Buffett Way involves a huge portion of educated guesses about the future competitive position of a company.

- “The difficulty is that we don’t know the factors that predict future sustainable high returns on invested capital.” (Tobias Carlisle).

- A structured decision-making process built on evidence-based quantitative factors is the best approach to investing unless you have Buffett’s genius.

- See how IBM fares according to the FALCON Method.

Nobody is infallible. Not even Warren Buffett. He is an extraordinary investor who happily admits to making mistakes and predicts this to continue as long as he lives. This article is not about crucifying him (for something that might not be a mistake at all) but to draw valuable conclusions from his latest comments on Berkshire’s IBM (NYSE:IBM) investment.

Could be a mistake

In 2016 Buffett said his IBM investment “could be a mistake.” He has become much more articulate about his position lately:

“I don’t value IBM the same way that I did six years ago when I started buying, I’ve revalued it somewhat downward … When it got above $180 we actually sold a reasonable amount of stock.”

To understand what has changed we must have a quick look at how Buffett invests.

It’s all about those wide-moat companies

Warren Buffett is constantly looking for firms that have a competitive advantage, allowing them to earn a consistently high return on invested capital. This advantage (the moat around the castle) must be sustainable so as to prevent competitors from invading the company’s market and pushing down profitability as a result.

Investing the Warren Buffett way requires a tremendous amount of industry knowledge and expertise in business analysis. This cannot be achieved without total devotion to lifelong learning.

“I read and read and read. I probably read five to six hours a day.” Warren Buffett

Here’s the problem (for most of us)

Capitalism is all about reversion to the mean. If a company is earning extra-high returns on invested capital, others will be attracted to its field. As soon as the newcomers put some money to work in that lucrative-looking market they can spoil the party by creating an oversupply. (And many other ways.) As competition intensifies rates of return tend to sink.

The problem is that investing the Warren Buffett way involves a huge portion of educated guesses about the future competitive position of the company. This is a really tricky part.

“It’s one thing to note post hoc that some companies did sustain high or low returns on capital over the period examined, and quite another to do it ex ante, or before the fact. The difficulty is that we don’t know the factors that predict future sustainable high returns on invested capital.” (Tobias E. Carlisle in his book Deep Value)

In fact, this is exactly what Warren Buffett seems to have got wrong, at least according to his latest remarks:

“I think if you look back at what they were projecting and how they thought the business would develop I would say what they’ve run into is some pretty tough competitors, IBM is a big strong company, but they’ve got big strong competitors too.”

Existing wide moats can be identified by sustained above average ROIC (return on invested capital). While observing the past is easy there is no easy-to-identify clue as to the future ROIC of a firm.

Even Warren Buffett makes mistakes (after having spent all his life reading) and unless you have his genius for business analysis your chances of predicting the future competitiveness of a company are rather slim. Based on this, paying elevated prices for current high ROIC is an investment strategy you most likely shouldn’t follow. Mean reversion pops its ugly head and takes care of your returns.

How to tackle this problem? An article is only as good as the meaningful and actionable takeaway it offers, so here are mine.

Takeaway for the individual investor

I am most certainly not like Warren Buffett. I am not spending all the day reading quarterly and annual reports simply because I do not enjoy doing that. Fortunately, this doesn’t mean I cannot achieve investment success. Let the man himself address this point:

“So the really big money tends to be made by investors who are right on qualitative decisions but, at least in my opinion, the more sure money tends to be made on the obvious quantitative decisions.” Warren Buffett, 1967

Buffett achieved his highest returns as a mostly quantitative investor before Phil Fisher and Charlie Munger influenced him to form his current style of investing which is not suitable for most of us (lacking Buffett’s extraordinary qualities and overwhelming devotion).

So what do I do?

After reading hundreds of investment books and gaining valuable (sometimes painfully expensive) experience I have figured out the following:

- A sensible investor should never follow any “guru” (even if he is called Warren Buffett) into any position. Blindly copying, coat-tailing others will make you vulnerable and stressful since you do not know what you are doing.

- You can never eliminate the uncertainty about a company’s future from investing. However there’s an intelligent way to address this. (Do not create a concentrated portfolio of stocks based on qualitative judgment unless your initials are W.B.)

- A structured decision-making process is the best approach to investing. I have built my process on evidence-based quantitative factors the combined use of which tilts the odds of superior performance in my favor. Investing is probabilistic and never deterministic, so this “odds tilting” is the best you can do.

- If you are not devoting your whole life to reading and investing, do not give too much room for qualitative decisions. It is complacent or outright crazy to believe that you will become the next Warren Buffett without making the same sacrifice he has made.

- Based on the above, I am utilizing an evidence-based investment process that is about 90% quantitative and 10% qualitative. I only let qualitative factors creep in when the field of stocks is narrowed down to such an extent it would be really hard to make a costly mistake.

- My process serves the construction of a buy-and-hold stock portfolio that is not highly concentrated. This portfolio produces dependable and growing passive income in the form of dividends while also having extraordinary total return potential thanks to the factually proven quantitative factors behind stock selection.

- I do not have to spend all my time with my investment decisions so I can live a meaningful life while employing a sensible approach to build wealth.

What about IBM in particular? If that stock ranks well in my all-round selection process (which it most certainly does at the moment) then I’m ready to buy a small position for my portfolio. My experience shows that most of these positions tend to work out really well, while only a few of them underperform. Picking stocks with the proven factors of outperformance and reliable dividend stream in mind can lead to great results on a portfolio level. And most importantly, it is a low-stress way: I don’t need to worry that Warren Buffett forgets to give me a ring next time he sells some of his positions I blindly followed him into…

A quick look at how IBM fares according to the FALCON Method

The FALCON Method is a structured stock selection process that serves the construction of a buy and hold portfolio with both an income and total return focus. The model is about 90% quantitative and 10% qualitative. The process includes the following steps.

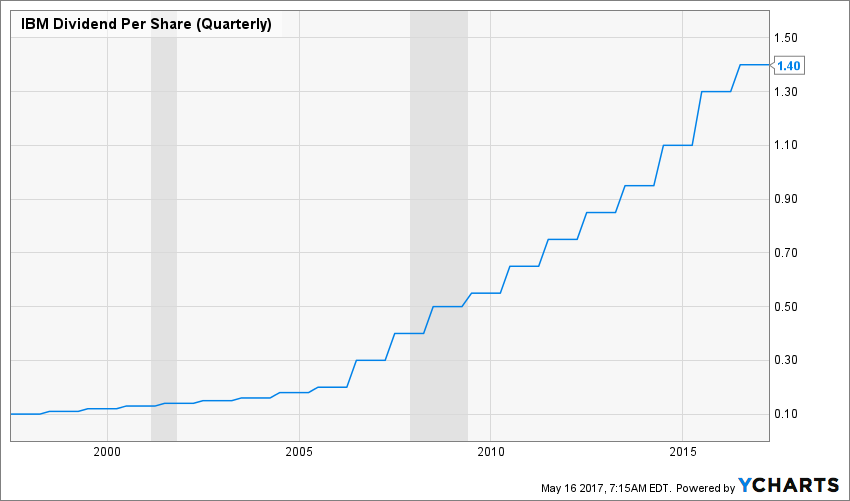

Step1: Narrow down the field of stocks. I focus on a group of stocks that tend to outperform according to historical data. My minimum requirement is 20 years of immaculate dividend history, meaning there are no dividend cuts within this period. IBM has been raising its dividend for 22 years now, so it passes easily.

Step2: Check the valuation. I focus on the stocks that seem to be undervalued historically based on various metrics. IBM looks to be available slightly on the cheap side of its historical valuation. Not a huge bargain I would say, but the current market does not offer too many quality stocks at fair or better prices. IBM passes this test as well.

| current | 3yr | 5yr | 10yr | 15yr | 20yr | |

| P/E | 11.0 | 12.2 | 10.4 | 11.9 | 12.8 | 15.5 |

| P/FCF | 11.6 | 12.4 | 11.9 | 12.9 | 13.3 | 16.9 |

| P/EBITDA | 7.7 | 8.6 | 7.2 | 7.6 | 7.7 | 8.6 |

Source: S&P Capital IQ, FAST Graphs

Step3: Three hurdles to filter them. I use absolute threshold criteria (dividend yield, free cash flow yield and shareholder yield) to determine whether a stock is good enough to invest my capital or I should pass up the opportunity. I deliberately define low limits with all the three indicators, since my experience shows that meeting all three low requirements together usually disqualifies a very large chunk of stocks on my list, but leaves just enough of them to continue the analysis. So this is a very tough combined filter in spite of seeming to be a bit lenient on the single factors. Again, IBM easily passes.

Step4: Rank the survivors. I’m using a multi-factor quantitative method ranking the factors of which are mostly Chowder-like numbers of different timeframes. IBM ranks 56th of the 322 stocks based on the combined “yield-plus-growth” indicators, yet when all the companies are excluded that fail to pass the three absolute threshold criteria or seem to be overvalued in historical comparison IBM becomes a Top 10 stock in the FALCON Method. (No surprise here: most top quality stocks are clearly overvalued today.)

Step5: Enter the human. This step involves some qualitative judgment but it is far from a Buffett-like deep analysis since not too many of us can carry that out at such a level and with that kind of confidence.

The company is earning high returns on invested capital, its dividend is more than adequately covered and playing with FAST Graphs gives me an estimated annualized rate of return between 8%-12% in the most conservative scenarios. For me, IBM near the $150 price level is clearly not a sell.